VISA Card Payment Methods India explained for 2026. Understand RBI monitoring, decline reasons, and how to reduce bank freeze risk with JeetBetter insights.

VISA Card – Payment Methods for Online Casino in 2026

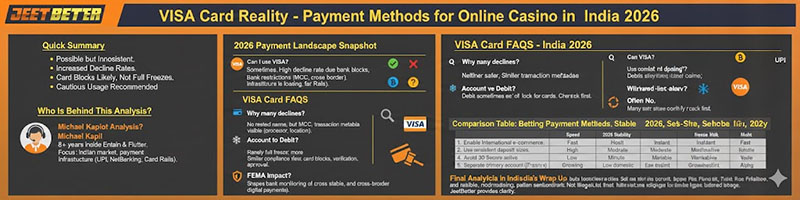

Quick Summary

In 2026, VISA card deposits for online betting in India remain possible but inconsistent. The Reserve Bank of India oversight framework and stricter bank monitoring increase decline rates and visibility. Freeze risk usually appears as card blocks rather than full account freezes. The safest practical approach is cautious usage, predictable deposit behavior, and understanding how cross border processing interacts with compliance systems.

Who Is Behind This Analysis?

This guide is authored by Michael Kapil, Senior Market Analyst and iGaming Strategy specialist .

Michael has spent eight years inside Entain and Flutter Entertainment, observing how operators manage Indian payment routing, fraud scoring, and account freeze waves. His work focuses specifically on Indian market localization and payment infrastructure behavior, including UPI, NetBanking, card rails, and cross border processors. What follows is not promotional commentary. It reflects observed banking behavior patterns, operator adjustments after GST restructuring, and card network friction in India facing betting environments.

What payment methods are available for online betting in India in 2026, and where does VISA fit?

If you are depositing on offshore online casinos or sports betting platforms in India in 2026, you will usually see UPI, NetBanking, wallet intermediaries, prepaid vouchers, crypto, and sometimes VISA card options. VISA sits in a secondary role. It works occasionally, but stability is lower compared to domestic rails like UPI Casino deposit.

Snapshot of 2026 Payment Landscape

- UPI remains the dominant deposit method

- Direct bank transfer still exists but carries freeze sensitivity

- E wallets such as Paytm or PhonePe are inconsistently supported

- Crypto is used by a smaller but risk aware segment

- VISA is available on some Curacao licensed operators

The Reserve Bank of India has not legalized gambling transactions. Instead, banks operate under risk control frameworks shaped by RBI AML guidance, FEMA considerations, and internal fraud scoring models. VISA transactions often route through overseas processors. That cross border element increases friction. From an operator perspective, card rails carry higher chargeback risk. From a bank perspective, gambling coded merchants are monitored more aggressively than digital subscription services or e commerce. For very large withdrawals, most Visa users eventually transition to direct bank wire transfers to handle the volume

In my time analyzing Indian acquisition funnels, card acceptance rates fluctuate sharply depending on the issuing bank. Public sector banks show higher decline rates compared to some private issuers. But even private banks dynamically adjust risk thresholds during what I call freeze waves, periods where monitoring tightens after regulatory commentary or enforcement noise.

Practical takeaway: VISA is usable, but it should not be your only payment method in 2026. Always check withdrawal compatibility before depositing.

Can I use a VISA card to deposit on online casino and betting sites in India in 2026?

Yes, sometimes. But acceptance depends on your issuing bank, international transaction settings, and the operator’s payment processor.

Direct Insight

- International e commerce must be enabled

- 3D Secure authentication must pass

- The processor must not be blocked by your bank

- Merchant category code may be restricted

Most India facing betting sites do not process directly under their brand name. Payments are routed through intermediary processors, often incorporated offshore. Statements rarely show the casino name. Instead, you will see a merchant descriptor linked to a foreign billing entity.

Banks do not rely only on descriptor text. They evaluate:

- Merchant category codes

- Country of settlement

- Transaction frequency

- Behavioral patterns

Under RBI expectations, banks must monitor unusual transaction behavior. A single small card deposit is unlikely to trigger escalation. Repeated cross border payments within short intervals increase scoring weight. When working inside acquisition teams at global operators, we often saw acceptance rates swing 15 to 20 percent based purely on issuer level rule changes. The player assumes the casino blocked them. In reality, the issuer declined the merchant.

Practical takeaway: Treat VISA as conditional access. Always confirm inside the cashier before planning large deposits.

Why do VISA card deposits to betting sites get declined so often in India?

Declines usually occur because issuing banks block gambling coded merchants or high risk processors. It is rarely a technical failure. It is automated risk management.

Common Decline Drivers

- Gambling merchant category restriction

- Cross border risk scoring

- Disabled international usage

- 3D Secure authentication failure

- Dynamic fraud prevention trigger

Indian banks operate under a conservative compliance posture. After GST Council restructuring of real money gaming taxation to 28 percent at the deposit level, payment scrutiny tightened indirectly. Operators adjusted routing strategies. Banks responded with more aggressive merchant filtering. From experience reviewing decline logs at operator level, repeated small rapid deposits look similar to card testing fraud patterns. Even legitimate users can be flagged if behavior resembles fraud signals.

Another factor is processor instability. Some offshore processors lose acquiring relationships. When that happens, transactions authorize but fail capture, leading to pending holds that disappear. The Reserve Bank of India does not issue public lists of blocked merchants. Each bank manages its own risk appetite.

Practical takeaway: If a deposit fails, do not retry repeatedly in rapid succession. That increases fraud scoring and may cause a card block.

Will my bank statement show gambling if I deposit with a VISA card?

It usually does not show the casino brand name. But it still creates visible transaction metadata.

Visibility Factors

- Merchant descriptor

- Country of transaction

- MCC code

- Frequency pattern

- Amount clustering

Statements often show processor entities rather than the gambling platform name. However, compliance systems analyze deeper transaction layers. Repeated deposits to the same overseas merchant code are easy to detect. Banks also analyze behavioral shifts. If a customer historically spends domestically and suddenly begins multiple overseas digital service payments, the risk profile changes.

Under FEMA sensitivity, international digital payments receive closer scrutiny. It does not mean legal action occurs. It means monitoring increases. In freeze cases I reviewed during 2022 to 2024 waves, full account freezes were rare from card usage alone. More common was temporary card disablement or additional KYC request.

Practical takeaway: VISA deposits are high visibility compared to crypto. If privacy sensitivity is a concern, understand that card rails are traceable and recorded.

Can my bank account be frozen because I used a VISA card for betting deposits?

Yes, but full account freezes are less common than card blocks. Most incidents involve temporary restriction pending clarification.

What Usually Happens

- Card transaction blocked

- Card temporarily disabled

- Bank calls for verification

- Rarely, debit freeze pending review

Under RBI AML expectations, banks must respond to unusual activity. However, a single isolated deposit rarely escalates. Patterns matter more than one transaction. In freeze waves observed during regulatory noise around online gaming taxation, banks became more cautious. Users with high frequency cross border card deposits were more likely to receive compliance queries. Operators also respond to chargeback risk. If a bank sees a high dispute rate linked to certain processors, it may proactively restrict further payments to those merchant IDs.

Practical takeaway: Avoid mixing high risk betting deposits with your primary salary account card if disruption would create inconvenience.

Is it safer to use a VISA credit card or VISA debit card for betting payments?

Neither offers structural safety advantage in compliance visibility. Both are scored under similar risk systems.

Differences in Practice

- Credit cards may allow dispute claims

- Debit cards pull directly from account balance

- Issuer policies vary widely

- Some banks restrict credit cards more aggressively

Credit cards can provide temporary liquidity and formal dispute processes. However, gambling transactions are often excluded from standard chargeback protections if authorized correctly. From an operational standpoint, debit cards sometimes show slightly higher approval rates because they are tied directly to deposit balances rather than credit risk evaluation. But this is bank dependent. Compliance monitoring does not differentiate meaningfully between debit and credit in gambling category scoring.

Practical takeaway: Choose based on issuer policy reliability, not perceived compliance safety.

Can I withdraw winnings back to the same VISA card in India?

Often no. Many offshore betting sites treat VISA as deposit only for Indian users.

Withdrawal Reality

- Card refunds depend on processor support

- Some issuers reject inbound gambling refunds

- Alternative withdrawal methods often required

Before depositing, always check the withdrawal page. In many cases, withdrawals route through bank transfer, e wallet, or crypto. Operators licensed under Curacao frameworks frequently rely on third party processors that support deposit only card functionality. Withdrawal compatibility matters more than deposit convenience.

Practical takeaway: Confirm exit route before funding. Deposit method does not guarantee withdrawal method.

How does FEMA affect VISA betting transactions in India?

FEMA influences how banks evaluate cross border digital payments. It does not directly criminalize individual card usage for offshore digital services. But it shapes monitoring intensity.

Key Considerations

- Overseas settlement increases compliance review

- High frequency cross border payments trigger alerts

- Banks may request transaction explanation

The Ministry of Finance periodically clarifies positions on foreign remittances and digital payments. While individual betting deposits are rarely escalated beyond bank level review, cross border clustering patterns increase friction. From operator side, routing strategies adapt to maintain acquiring stability. When certain acquiring banks become restricted, processors switch entities. That can temporarily increase declines.

Practical takeaway: Keep international card limits transparent and consistent. Unexpected spikes increase friction.

Comparison Table: Betting Payment Methods in India 2026

| Method | Speed | Freeze Risk | KYC Level | Reversal Risk | Best For | 2026 Stability |

|---|---|---|---|---|---|---|

| UPI | Instant | Moderate | Linked to bank | Low | Small frequent deposits | High but monitored |

| Bank Transfer | Hours | High | Full bank trace | Low | Larger withdrawals | Moderate |

| E Wallets | Fast | Moderate | Wallet KYC | Medium | Buffer layer use | Variable |

| Crypto | Minutes | Low domestic visibility | Exchange KYC | Irreversible | Privacy aware users | Growing |

| Prepaid Vouchers | Instant | Low | Minimal | None | Controlled spending | Limited availability |

| VISA Card | Instant if approved | Moderate card block risk | Bank linked | Chargeback possible | Backup method | Inconsistent |

How can I reduce bank risk when using a VISA card for betting deposits?

If you plan to use VISA, risk reduction is about behavior discipline, not secrecy.

Step by Step Risk Reduction

- Enable international e commerce intentionally

- Use consistent deposit sizes

- Avoid rapid repeated retries after declines

- Keep 3D Secure authentication active

- Maintain transaction records

- Separate primary salary account if risk sensitive

In operator compliance reviews I have analyzed, the majority of escalation cases involved erratic deposit patterns rather than steady moderate usage. Banks score anomaly more heavily than activity volume alone. The GST 28 percent operator burden has increased processor rotation in the market. That means merchant descriptors may change over time. Sudden unfamiliar overseas charges can prompt bank alerts. If your bank blocks gambling transactions on your Visa, we recommend using AstroPay prepaid cards as a reliable workaround

Practical takeaway: Stability of behavior reduces disruption more effectively than chasing alternative processors repeatedly.

Frequently Asked Questions About VISA Card as Payment Methods in India

Can I use a VISA card to deposit on online casino and betting sites in India in 2026?

Yes, you can sometimes use a VISA debit or credit card, but acceptance is inconsistent in 2026. Many India facing offshore sites route card payments through international processors, and Indian banks often block gambling coded transactions. Even when a deposit works, it is fully visible on your bank statement and can trigger monitoring under RBI and card network risk rules. Always confirm card acceptance inside the cashier before relying on it.

Why do VISA card deposits to betting sites get declined so often in India?

They are declined mainly because the issuing bank blocks the merchant category or the processor is flagged as high risk. Banks in India apply stricter controls on cross border card payments, and gambling related merchant codes are frequently restricted. Declines can also happen due to international usage limits, disabled e commerce settings, insufficient funds, or 3D Secure failures. If one site fails, it does not mean your card is broken. It often means the processor is blocked.

Will my bank statement show gambling if I deposit with a VISA card?

It usually will not show the casino brand name, but it can still look like a gambling related charge. Statements often show a payment processor, merchant descriptor, or overseas billing entity. Banks do not rely only on text. They also use merchant category codes, geography, and transaction behavior. If you make repeated deposits or large deposits, the pattern becomes obvious under monitoring systems. So card deposits should be treated as high visibility.

Can my bank account be frozen because I used a VISA card for betting deposits?

Yes, it is possible if the transaction pattern triggers compliance or fraud alerts. Banks monitor unusual international card spending under RBI AML expectations and internal risk systems. A single small deposit rarely causes a freeze, but repeated high frequency payments, sudden large amounts, or links to flagged processors can lead to temporary restrictions on card usage or account debits. The most common outcome is a card block, not a full account freeze.

Is it safer to use a VISA credit card or VISA debit card for betting payments?

Neither is automatically safer. Credit cards can have stronger dispute processes, but many Indian issuers restrict gambling coded merchants and may decline more often. Debit cards pull funds directly from your account, which can feel riskier if you want tighter control. From a compliance visibility standpoint, both are visible and scored similarly. The practical choice is usually whichever your bank allows for international online transactions, but many users find stability is low.

Can I withdraw winnings back to the same VISA card in India?

Sometimes, but many betting sites do not support card withdrawals for Indian users. Card payments are often deposit only, and withdrawals may be processed via bank transfer, e wallets, or crypto instead. Even if a site claims card withdrawal support, the processor and issuer must accept inbound refunds, which is not consistent. Before depositing, always check the withdrawal page and confirm your available methods, because the withdrawal rules matter more than the deposit method.

How long do VISA deposits take to reach my betting account?

If approved, VISA deposits are usually instant or within a few minutes. Delays typically come from 3D Secure verification, processor risk checks, or operator manual review. If your bank shows the transaction as successful but the betting wallet is not credited, capture the transaction reference and contact support fast. Card settlements can be reversed later if the processor fails compliance checks, so keep records until the credit is confirmed.

What is 3D Secure and why does it matter for VISA betting deposits?

3D Secure is an additional authentication step required by many banks for online card payments. In India, most VISA transactions require OTP or app based approval. If 3D Secure fails, the deposit will decline even if you have funds. Betting processors also trigger extra verification more often because the category is high risk. Make sure international e commerce is enabled, your phone is receiving OTP, and your bank has your correct number. Many declines are simply authentication failures.

Do VISA betting deposits trigger GST for players in India?

GST is applied at the operator level on real money gaming deposits under GST Council rules, not by VISA itself. Your bank does not add GST to the card payment. However, operators may adjust deposit value, bonuses, or wallet credits because of the 28 percent tax burden. From the player side, the key point is that using a VISA card does not change GST exposure. The tax impact shows up in how the operator structures deposits, not in your card statement.

Can VISA deposits trigger FEMA or international transaction compliance checks?

Yes, because many card deposits route to overseas processors. Banks apply international transaction risk monitoring and may question repeated cross border payments. This is where FEMA related sensitivity can appear indirectly through bank controls, not through direct notices to you. If your card is frequently used for overseas digital services, banks may ask for confirmation or block the merchant. Keeping your international limits and documentation in order reduces friction, but it does not remove monitoring.

What limits apply to VISA card deposits for betting in India?

Limits depend on your bank, card type, and international usage settings. Your bank may cap international online spending daily or monthly. Some users also hit per transaction limits or risk based caps that change dynamically. On the betting site side, processors may impose their own minimum and maximum deposit amounts. If you keep getting declines at a certain number, it may be an issuer limit rather than a site issue. Check your bank card settings first.

Are VISA betting deposits reversible if something goes wrong?

Sometimes, but reversals are not guaranteed and can take time. Card payments have dispute mechanisms, but banks may treat gambling related disputes differently and may not support chargebacks for authorized transactions. If you sent the money correctly and received betting credits, a reversal is unlikely. If the merchant did not credit you, you may have a stronger case. Keep screenshots, transaction IDs, and communication logs. Practical prevention is better than relying on chargeback.

Why do some betting sites ask for extra KYC when I use a VISA card?

Because cards increase fraud risk for operators. Chargeback risk, stolen cards, and mismatched identities are common problems. Operators often require that the cardholder name matches the betting account name and may ask for card verification steps. This can include masked card photos or proof of ownership. KYC is also needed for withdrawals, regardless of deposit method. If you want fewer payout delays, align your identity documents and avoid using someone else’s card.

Is using a VISA card more risky than UPI for betting deposits in India?

It is riskier in a different way. UPI is domestic and very traceable, while VISA deposits often route internationally and face higher decline rates and stricter bank blocks. From a freeze perspective, UPI triggers pattern monitoring, while cards trigger both fraud controls and cross border risk scoring. In practice, cards are less stable for deposits in 2026, but they can be useful when UPI is down. Risk is not lower, it is just structured differently.

Can I use a VISA card for betting without my bank blocking it?

Sometimes, but it depends on your issuing bank’s risk policy. Many banks block gambling coded merchants by default. You can improve success rates by enabling international e commerce, confirming your 3D Secure setup, and avoiding repeated rapid deposits. Even with everything enabled, your bank can still decline transactions to certain processors. This is not personal. It is automated risk control. If your bank repeatedly blocks the same merchant, it usually will not change without policy shifts.

Why do VISA transactions sometimes show as pending then disappear?

This happens when an authorization is placed but the transaction is not captured. Your bank may show a pending hold, then release it if the merchant or processor fails to complete the charge. Betting processors often run risk checks after authorization, and if they reject it, the hold may drop in a day or two. This is common in high risk categories. If you see many pending holds, it is a sign the processor is unstable or your bank is rejecting capture.

Can I use a virtual VISA card for betting deposits in India?

Sometimes, but many processors block virtual cards because they are linked to higher fraud and chargeback rates. Virtual cards can also trigger extra verification steps. If you use one, expect lower acceptance and higher KYC requests. Also, withdrawal back to a virtual card is usually not supported. The practical rule is to treat virtual VISA as deposit only, and confirm withdrawal methods before funding. Stability depends heavily on the processor and issuer.

What should I do if a VISA deposit is charged but my betting account is not credited?

First, do not repeat the payment immediately. Capture your transaction reference, screenshot the bank message, and check if the deposit shows as pending in the betting cashier. Then contact operator support with the transaction ID and time. If the operator cannot locate it, contact your bank and ask whether it is authorized or captured. Many cases resolve as a reversed authorization. Keeping clean evidence helps you resolve it faster.

How do I reduce bank risk when using a VISA card for betting deposits?

Use predictable behavior and keep your banking setup clean. Enable international e commerce only if needed, avoid rapid repeated deposits, and do not use your main salary card if you are worried about disruption. Keep deposit sizes consistent and maintain records. If your bank flags you, respond calmly and provide accurate information. The goal is not to hide activity, but to avoid triggering fraud patterns that look like card theft or money movement under RBI monitored systems.

Is VISA still a viable payment method for Indian betting in 2026?

Yes, but it is less reliable than UPI for most users. Acceptance depends on the operator’s processor, bank policy, and cross border transaction controls. VISA can work as a backup when UPI is unstable, but it should not be the only method you rely on. Expect higher decline rates, more KYC friction, and limited withdrawal support. Treat it as a high visibility, moderate stability payment rail in the 2026 Indian betting market.

Final Analytical Wrap Up

In 2026, VISA card deposits remain part of the Indian online betting ecosystem, but they operate under increased monitoring shaped by Reserve Bank of India oversight, Ministry of Finance sensitivity around cross border flows, and operator compliance restructuring after GST reform.

Card rails are visible, moderately stable, and sensitive to pattern-based scoring. They are not illegal by default. But they are not frictionless either. Understanding how banks monitor merchant codes, how processors rotate acquiring entities, and how behavioral patterns trigger alerts is essential.

Payment awareness and disciplined usage reduce disruption. Regulatory uncertainty continues to shape routing behavior. JeetBetter’s approach is not to encourage risk, but to provide clarity so Indian players understand how these payment systems actually function in 2026. Recommended online casino for Visa card deposits and withdrawal are: 10Cric Casino and Rajabet Casino

Top – Indian Casinos

150% Welcome Bonus up to ₹40,000

Welcome bonus offering 100% up to €600/$600

350% bonus of up to ₹70,300

Get 200% Welcome Bonus up to ₹1 Lakh + ₹500 Free Bet

Get 100% up to ₹25,000 bonus on your first deposit.

200% welcome bonus on their first deposit up to ₹1,00,000

Top Rated Casinos

200% welcome bonus on their first deposit up to ₹1,00,000

Get 200% Welcome Bonus up to ₹1 Lakh + ₹500 Free Bet

Get 100% up to ₹25,000 bonus on your first deposit.

150% Welcome Bonus up to ₹40,000

Welcome bonus offering 100% up to €600/$600

350% bonus of up to ₹70,300