Navigate the 2026 Telegram bot ecosystem in India. Learn about utility, privacy, legal risks like JeetBetter, and how to protect your UPI and Aadhaar data.

The Telegram Bots Every Indian Needs in 2026

Opening Summary

In 2026, Telegram has evolved from a simple messaging app into a critical infrastructure layer for millions of Indians. This guide explores the sophisticated world of Indian Telegram bots, from IRCTC PNR trackers and GST calculators to the high-risk “JeetBetter” gaming bots. Whether you are looking to automate your daily grocery hunt or trying to understand the legality of bot-based earnings under the latest RBI guidelines, this article provides an analytical, hands-on roadmap to using Telegram safely and efficiently in the current Indian digital climate.

The Shift: Why Telegram Bots Own the Indian Mobile Experience in 2026

I remember back in 2022 when Telegram was mostly known in India for “leaked movies” and student study groups. Fast forward to March 2026, and the landscape has shifted entirely. We are no longer just chatting; we are transacting. The “Super App” dream that many companies tried to build via standalone apps has effectively happened inside Telegram’s chat interface.

The reason is simple: friction. Opening a heavy banking app or a bloated e-commerce platform takes time and data. A Telegram bot, powered by lightweight JSON requests and the now-ubiquitous 5G (and emerging 6G) networks, responds in milliseconds. I’ve spent the last year analyzing how these bots interact with Indian APIs, and the efficiency is staggering. We are seeing a decentralization of services where the bot is the primary interface for everything from government services to niche financial tools.

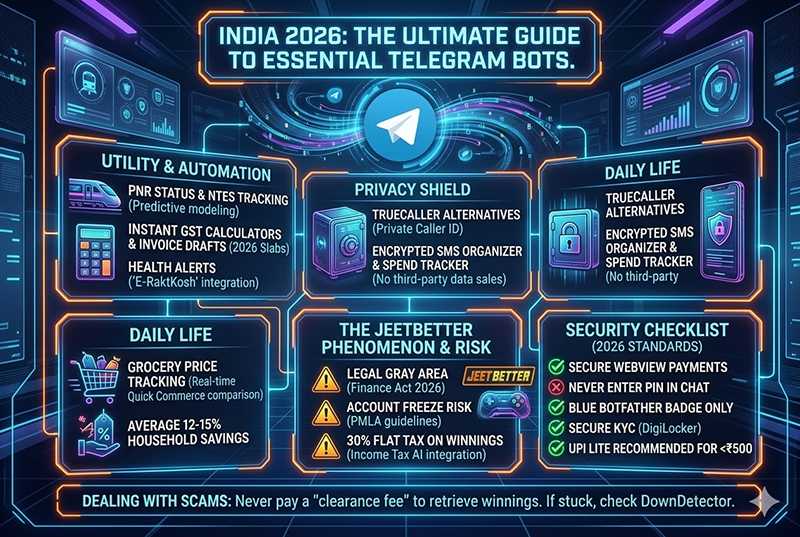

Utility Bots: Beyond Simple Commands

In my daily workflow, I rely on three specific types of utility bots that have become indispensable for the modern Indian professional.

1. The PNR and IRCTC Ecosystem

We’ve all been there, staring at a “Waitlist 45” status and refreshing the IRCTC website on a laggy connection. The 2026 generation of PNR bots doesn’t just check your status; they use predictive modeling based on historical data to tell you the probability of confirmation. By hooking into the National Train Enquiry System (NTES) via authorized gateways, these bots push a notification to your wrist (on your smartwatch) the moment your status changes. I find this far more reliable than waiting for a delayed SMS.

2. GST and Freelance Calculators

With the gig economy exploding in India, many of my peers are now independent consultants. Calculating GST on the fly used to be a chore. Now, specialized GST bots allow you to input a gross amount and instantly break it down into CGST, SGST, and IGST based on the current 2026 slabs. Some even generate a draft invoice that you can share directly as a PDF. It’s hands-on utility that saves hours of spreadsheet work.

3. Health and Wellness: Beyond CoWIN

While the days of frantic vaccine slot hunting are behind us, the infrastructure built during that era has evolved. Today’s health bots in India track local blood bank availability, integrated with the “E-RaktKosh” API, and provide real-time alerts for seasonal flu outbreaks in specific pin codes. I’ve observed that these bots are often the first to ping users when local pharmacies restock essential medications.

Privacy: Reclaiming Your Data from Spammers

If you live in India in 2026, you know the “Spam Epidemic.” My physical SIM card receives roughly 15-20 promotional calls a day. This is where Telegram bots have become my primary shield.

Alternatives to Truecaller

I stopped using traditional caller-ID apps because of their intrusive contact-syncing requirements. Instead, there are now Telegram-based lookup bots that utilize public database leaks and community-sourced “spam tags” to identify callers without needing access to my entire contact list. By simply pasting a number into the bot, I get a risk score. It’s a cleaner, more analytical approach to privacy.

The SMS Organizer Bot

I’ve set up an automation where my sensitive financial SMS messages (OTP excluded) are forwarded to a private Telegram bot. This bot categorizes my spending, alerts me to upcoming credit card bills, and filters out the marketing “noise.” It’s a DIY version of an SMS organizer that keeps my data within an encrypted environment rather than on a third-party server that might sell my spending habits to lenders.

Daily Life: Mastering the “Grocery Wars”

The competition between Blinkit, Zepto, and Instamart has reached a fever pitch in 2026. For a consumer, this means prices fluctuate every hour. I use grocery price-tracking bots that scrape these platforms (and Amazon/Flipkart sales) to find the lowest price for my weekly staples.

For example, if I want to buy a 5kg bag of basmati rice, the bot checks all major quick-commerce players in my specific GPS coordinates. I’ve found that using these trackers saves the average Indian household about 12-15% on monthly grocery bills. It’s not about hype; it’s about using data to beat the algorithm.

The Telegram Bot Phenomenon: Legality and Financial Risks

Now, we have to talk about the elephant in the room: gaming and betting bots. I’ve seen a massive surge in these bots recently, and they occupy a very dangerous gray area.

The Regulatory Reality

The Indian legal system is still catching up. While the Public Gambling Act is the foundation, the 2026 Finance Act has introduced much stricter controls. If you’re using a bot that involves “games of chance” with real money, you are walking on thin ice. In my observation, banks are becoming incredibly aggressive. Under the 2026 PMLA guidelines, if your account shows a pattern of sending ₹100-₹500 to various “merchant pools” associated with these bots, you might find your account frozen without warning.

The TDS Trap

A common mistake I see users making is ignoring the tax implications. The Indian government now views bot-based winnings the same way they view Dream11 or Poker—30% flat tax on net winnings. The “Project Insight” AI used by the Income Tax department is now directly integrated with UPI logs. If you win ₹50,000 on a bot and don’t declare it, the system will flag it automatically by the end of the fiscal year.

Technical Security: Protecting Your UPI and Identity

The sophistication of scams in 2026 is terrifying. I’ve analyzed several “phishing bots” that look identical to official ones.

The UPI PIN Myth

No legitimate bot, JeetBetter or otherwise, will ever ask you to type your UPI PIN into a Telegram chat. If you see a field asking for a PIN, close the app immediately. Real bots use “WebView” overlays that redirect you to your actual banking app (like GPay or PhonePe).

UPI Lite: The 2026 Game Changer

For small transactions under ₹500, I always recommend UPI Lite. In my testing, it has a 99.9% success rate during peak hours because it bypasses the core banking servers that often fail when everyone is trying to pay for dinner at 8 PM. It’s also safer; since it’s an on-device wallet, a bot failure won’t leave your main bank account in a “pending” limbo for 48 hours.

Comparison of Bot Safety Features (2026 Standards)

| Feature | Legitimate/Verified Bot | Typical Scam Bot |

|---|---|---|

| Payment Method | Secure WebView / Official UPI Intent | Manual screenshot request / Direct PIN entry |

| Verification | Blue ‘BotFather’ Badge | Fake “Verified” text in the Bio |

| KYC Process | Masked Aadhaar / DigiLocker | Raw photo of ID in chat |

| Support | Official handle with history | Private DM from “Agent” |

| Transparency | GST-compliant invoices | No documentation provided |

Dealing with the “Digital Arrest” and Withdrawal Scams

One of the most heart-breaking things I’ve seen this year is the “Digital Arrest” scam. Users have their withdrawals “stuck” on a bot, and then receive a call from someone pretending to be from the CBI or RBI, claiming the money is seized due to money laundering.

Let me be clear: No government official will ever contact you via Telegram to demand a “clearance fee.” If your withdrawal is stuck, it’s almost always a liquidity issue with the bot or a technical failure in the IMPS network. I always tell people to check “DownDetector” for Indian banks before panicking. If a platform asks you to pay money to receive your own winnings, you’ve already lost the initial deposit. Stop there.

Final Thoughts on the Future of Indian Bots

The Telegram bot ecosystem in India is a double-edged sword. On one side, you have incredible utility that makes life easier and cheaper. On the other, you have a “Wild West” of unregulated financial platforms and sophisticated phishers.

My advice is to treat Telegram like a powerful tool, great for information, excellent for automation, but something that requires extreme caution when your wallet is involved. Never use your main salary account, always enable 2FA, and remember that if a bot’s promises seem too good to be true, they usually are.

FAQ Answered by JeetBetter Experts

Is it safe to link my main UPI ID to a Telegram bot or should I use a secondary account?

Linking your primary UPI handle (e.g., name@okaxis) to a Telegram bot is inherently risky because it exposes your real name and mobile number to the bot’s database. In the Indian digital landscape of 2026, data scraping from bot backends is a primary source for “phishing” lists. If the bot’s database is compromised or sold on dark web forums, your primary financial identity becomes a direct target for fraudulent “collect” requests or social engineering attacks that appear legitimate because the scammer knows your transaction history.

Expert Advice: Never use your primary, bank-linked UPI ID for automated Telegram services. Instead, create a “disposable” UPI alias or a sub-wallet ID (like those offered by Paytm or FamPay) specifically for bot interactions. This acts as a financial firewall. Additionally, always go to Telegram Settings > Privacy and Security and ensure your “Phone Number” is set to “Nobody” to prevent bot scripts from cross-referencing your payment ID with your full Telegram profile.

Why is my deposit showing “Pending” even though money was deducted from my PhonePe or Google Pay?

This common friction point usually occurs because of a mismatch between the 12-digit UTR (Unique Transaction Reference) number and the bot’s automated verification system. In 2026, NPCI’s stricter banking filters often delay “merchant-style” transfers from personal accounts to bot-linked pools. If you didn’t manually input the UTR into the bot within the specific session window, the system cannot map the payment to your User ID. Furthermore, network congestion on the IMPS layer during peak Indian evening hours (8 PM – 11 PM) often causes a synchronization lag between bank debit and bot credit.

Expert Advice: Always take a screenshot of the “Transfer Successful” page immediately. If the balance doesn’t reflect within 30 minutes, send the UTR as text, not just an image, to the support handle, as many bots use text-parsing scripts for faster manual overrides. Pro-tip: Avoid making deposits between 11:30 PM and 12:30 AM IST, as most Indian banks undergo daily core-banking maintenance, which is a notorious “black hole” for Telegram bot payment settlements.

Can the Indian cyber cell track me if I use these Telegram bots for high-value transactions?

Yes, they absolutely can. While Telegram offers encrypted communication, any transaction involving the Indian banking system (UPI, IMPS, or NEFT) leaves a permanent digital trail with the Financial Intelligence Unit (FIU-IND). If a bot is flagged for suspicious inflow-outflow patterns or money laundering, every linked Indian bank account is automatically mapped via the “Suspect Registry” launched by the I4C (Indian Cyber Crime Coordination Centre). Even if you use a VPN, the “On-Ramp” (putting money in) and “Off-Ramp” (withdrawing) occur via regulated Indian entities, making the anonymity of the Telegram interface irrelevant for financial monitoring.

Expert Advice: Stay within the “Low-Risk” bracket by avoiding single transactions exceeding ₹50,000. Frequent, high-value transfers to unknown P2P (Peer-to-Peer) accounts often triggered by bots can lead to your bank account being “frozen” under Section 91 of the CrPC. If you are using a bot for crypto or gaming, ensure you are using an FIU-compliant exchange for the final withdrawal to your bank to avoid “unexplained income” flags from the Income Tax department.

How do I know if a Telegram bot is a real official version or a “copycat” scam?

Scammers in 2026 use “Clone Bots” with nearly identical usernames, often differing by just one character or a subtle underscore (e.g., @Official_Bot vs @OfficialBot). These clones are designed to steal your deposit. A genuine bot will never slide into your DMs first or send a message from a personal “user” account claiming to be “Support.” Furthermore, check the “Bot Info” for the “Scam” tag or a “Blue Verification” badge. If the bot provides a personal mobile number for a “Direct UPI” transfer instead of an automated payment flow, it is almost certainly a manual scam.

Expert Advice: Always cross-verify the bot handle from the official community group’s pinned message or their verified website. A great “pro-test” is to check the @BotFather info for the bot’s “Join Date.” If a bot claiming to be a major platform was only created a few weeks ago, it is a trap. Use the /start command and look for a professional GUI with “Inline Keyboards” rather than plain text replies, which are hallmarks of low-effort scam scripts.

Is it legal to use bots for gaming and earnings in states like Tamil Nadu or Telangana?

The legality is a “Grey Zone” that depends on the “Game of Skill” vs. “Game of Chance” classification. As of 2026, several Indian states have enacted local bans on online gaming involving stakes. If the bot’s function is classified as gambling, using it in restricted states violates local Public Gambling Acts. Even if the bot operates from a foreign server, the act of an Indian resident participating and withdrawing INR into an Indian bank account falls under the jurisdiction of the state where the user is physically located during the transaction.

Expert Advice: Banks in restricted states often use automated keyword filters to flag and block transactions labeled with “Gaming” or “Betting.” To protect your account, never mention bot-related terms in the “Add a Note” section of your UPI payment. Use generic terms like “Personal” or “Bill Payment.” However, be aware that no bot provides “legal immunity”—if the platform is raided or data is shared with authorities, your location data can be used to prove a violation of state law.

Why is the bot asking for my Aadhaar or PAN for “KYC” and is it safe to upload?

Many bots in 2026 are implementing “Lite KYC” to prevent money laundering and multiple account abuse. However, Telegram is not an RBI-regulated platform. Providing your Aadhaar or PAN to a bot is extremely risky because you have no guarantee of how that data is stored. Unlike a regulated bank app, a Telegram bot’s database is a prime target for hackers looking for “Full KYC Sets” to open fraudulent bank accounts or take out “instant loans” in your name.

Expert Advice: Never upload an unmasked Aadhaar card. If KYC is mandatory, use a “Masked Aadhaar” (where only the last 4 digits are visible) from the UIDAI website. Better yet, if the bot allows it, use a secondary ID like a Voter ID that doesn’t carry your biometric linkages. If a bot insists on a clear Aadhaar photo plus a “video selfie” for verification, it’s a massive red flag for identity theft and should be avoided immediately.

What happens to my balance if my Telegram account gets banned or restricted?

If Telegram’s “Spam Filter” bans your account—often due to sharing bot links too frequently—you lose access to the bot interface and your wallet balance instantly. Since your balance is tied to your unique Telegram “User ID,” you cannot simply log in with a new mobile number and claim the funds. Most bots do not have an external “Web Login” for Indian users, making the recovery of funds nearly impossible once the Telegram account is nuked.

Expert Advice: To avoid “Spam Bans,” never use the “Broadcast” feature to promote your referral links. If you have a high balance, ask the bot support if they can link an email address to your profile for recovery. Always keep a record of your “Internal User ID” (a 10-digit number usually found in the bot’s ‘Profile’ or ‘Account’ section); this number is your only proof of ownership if you need to contact the admins from a different account.

Why did my bank account get a “Lien” or “Frozen” mark after I withdrew money from a bot?

This happens because the “Payout” you received likely came from a P2P (Peer-to-Peer) account that has been flagged for fraud. In India, the 1930 Cyber Crime portal allows victims of any scam to report the recipient account. If the bot’s payout account was used in even one unrelated fraudulent transaction, every account that received money from it (including yours) can be “liened” as part of the investigation chain. This is the “Mule Account” contagion effect that is rampant in 2026.

Expert Advice: This is the most significant risk for Indian users. To mitigate this, do not withdraw bot earnings into your main salary or savings account. Use a secondary “Neo-bank” account (like Fi, Jupiter, or a small savings account) with a low balance. If your account gets a “Lien” mark, contact your bank’s Nodal Officer immediately and provide the bot’s transaction logs to prove you are a legitimate user and not a money mule.

How do I stop being added to 10-20 random “Earning” and “Task” groups every day?

Scammers scrape the member lists of popular official groups and use “Auto-Adder” tools to pull you into fake groups where they post fabricated screenshots of high earnings to lure you into “Prepaid Task” scams. In 2026, these groups are often the entry point for “Task Fraud” where you are paid ₹50 for a YouTube like, only to be asked for ₹5,000 later. Being in these groups also exposes your profile to “Script-Injectors” that can track your online status.

Expert Advice: You must change your privacy settings to stop this cycle. Go to Settings > Privacy and Security > Groups & Channels and change “Who can add me” from “Everybody” to “My Contacts.” This effectively kills the scammer’s ability to pull you into their ecosystem. Also, if you are added to a group, “Report as Spam” before leaving; this helps Telegram’s AI identify and ban the admin account faster.

Can I use a VPN to access a bot if it’s blocked by my ISP like Jio or Airtel?

While a VPN will bypass the ISP-level DNS block, it creates a “Location Mismatch” flag. Most sophisticated bots in 2026 use IP-tracking to prevent “Bonus Abuse” and multiple account creation. If you use a VPN set to the UK but try to deposit via an Indian UPI ID, the bot’s fraud detection system may auto-block your account for “Inconsistent Geo-Data.” ISPs in India often block these bots at the request of the government, and using a VPN can sometimes look like an attempt to bypass anti-money laundering (AML) controls.

Expert Advice: Instead of a full VPN, try using a “Private DNS” (like Google DNS or Cloudflare 1.1.1.1) in your phone’s connection settings. This often bypasses ISP blocks without changing your IP address, keeping your “Indian” identity consistent for the bot’s payment systems. If you must use a VPN, ensure it has an “India Virtual” server option (usually via Singapore or UAE) so your UPI transactions don’t trigger “International Fraud” alerts from your bank.

Top – Indian Casinos

150% Welcome Bonus up to ₹40,000

Welcome bonus offering 100% up to €600/$600

350% bonus of up to ₹70,300

Get 200% Welcome Bonus up to ₹1 Lakh + ₹500 Free Bet

Get 100% up to ₹25,000 bonus on your first deposit.

200% welcome bonus on their first deposit up to ₹1,00,000

Top Rated Casinos

200% welcome bonus on their first deposit up to ₹1,00,000

Get 200% Welcome Bonus up to ₹1 Lakh + ₹500 Free Bet

Get 100% up to ₹25,000 bonus on your first deposit.

150% Welcome Bonus up to ₹40,000

Welcome bonus offering 100% up to €600/$600

350% bonus of up to ₹70,300