Paytm India betting guide for 2026. Understand RBI monitoring, wallet freeze risk and safer deposit practices with JeetBetter insights.

Paytm Casino for Online casino and Sport betting Sites

Quick Summary

Paytm can be used for online casino and sports betting deposits in India in 2026, primarily through UPI or linked wallet transfers. However, transactions remain fully traceable under Reserve Bank of India oversight. Account freezes typically occur due to transaction patterns, not a single deposit. The safest practical approach involves controlled transaction sizes, consistent KYC compliance, and understanding GST and banking monitoring realities.

What is Paytm’s role in online betting payments in India

Paytm for Online Casino and Sports Betting in 2026?

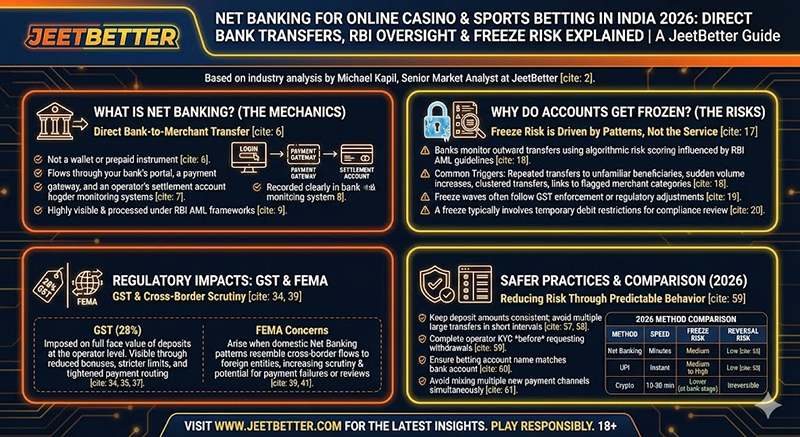

Paytm acts primarily as a UPI interface or regulated wallet intermediary rather than an independent gambling payment system. In 2026, most betting deposits through Paytm are processed via UPI rails governed by NPCI and monitored under RBI frameworks. It does not function as a private or offshore payment bypass.

To understand Paytm’s role, you must separate perception from infrastructure. Many players assume Paytm operates independently from banks. In reality, Paytm is tightly integrated into India’s formal financial ecosystem. Wallet balances, UPI handles, and linked bank accounts are all subject to RBI regulated AML oversight. Paytm also functions as a VPA, allowing you to use it on various UPI-enabled gambling platforms across India

From my time observing operator payment routing strategies at Entain and Flutter, I saw how Indian wallet integrations evolved. Around 2021 to 2023, operators aggressively onboarded UPI based solutions to localize deposits. By 2024, banks began tightening merchant monitoring, particularly where gambling category routing appeared through indirect gateways.

By 2026, Paytm works in three main betting scenarios:

- UPI transfer to a virtual payment address provided by the operator.

- Wallet based merchant payment routed through a payment aggregator.

- Indirect transfer through a gateway rotating VPAs or QR codes.

None of these structures remove regulatory visibility. They simply change the routing layer. The Ministry of Finance has repeatedly clarified that digital wallet transactions fall within formal monitoring frameworks. So Paytm should be viewed as a compliant financial interface, not a grey zone tool. If you have a linked bank account but no wallet balance, you might find GPay for online casinos to be a more convenient choice

Is Paytm safe for casino deposits under RBI rules?

Paytm is safe from a platform integrity perspective, but not invisible under RBI compliance monitoring. All wallet and UPI transactions fall within AML and suspicious transaction reporting obligations. Safety depends on usage patterns rather than the brand itself.

The Reserve Bank of India requires regulated payment providers to monitor unusual transaction flows. That includes repetitive transfers to high risk merchant clusters. In 2023 and 2024, the GST Council’s 28 percent tax decision on real money gaming increased compliance scrutiny across operators. By 2026, banks and wallet providers apply tighter pattern recognition.

Safety therefore has two components:

- Technical safety. Paytm is secure, encrypted, and regulated.

- Compliance exposure. Transactions remain traceable and reviewable.

During the account freeze waves observed in late 2023 and early 2024, most disruptions were triggered by transaction frequency spikes and circular payment flows, not by one isolated deposit.

If a user makes occasional small deposits, the risk profile is different from a user making rapid repeated transfers. The difference lies in behavioral analytics, not the payment app.

Can Paytm cause bank account freezes for betting transactions?

Yes, Paytm linked accounts can face temporary freezes if transaction patterns trigger compliance flags. The freeze risk arises from AML monitoring by banks and payment aggregators, not from Paytm itself.

Banks analyze:

- Sudden transaction volume spikes

- Repeated transfers to similar VPAs

- Round trip patterns involving withdrawals

- Cross linkage between multiple betting platforms

Under RBI AML circulars, suspicious transaction reporting is mandatory for unusual activity. In practice, freezes are precautionary reviews. They are rarely permanent closures unless broader irregularities exist.

In my experience analyzing payment data for Indian markets, freeze waves typically follow:

- Regulatory announcements

- GST enforcement updates

- Publicized investigations

- Payment gateway shutdowns

For example, when aggregator relationships shift, merchant routing patterns change rapidly. Users continuing high volume transfers during such shifts are more likely to encounter temporary restrictions. The safest behavioral approach is consistency and moderation rather than assuming any wallet provides protection.

How does Paytm compare to UPI, Net Banking, and crypto for betting?

Paytm largely operates through UPI infrastructure, making it similar in traceability to Google Pay or PhonePe. Crypto differs structurally but introduces separate compliance layers at exchanges.

Below is a comparative overview:

| Method | Speed | Freeze Risk | KYC Level | Reversal Risk | Best For | 2026 Stability |

|---|---|---|---|---|---|---|

| UPI via Paytm | Instant | Medium | Full KYC | Low | Small deposits | High |

| Direct Net Banking | Instant to few hours | Medium to High | Full KYC | Low | Larger transfers | Moderate |

| E Wallets | Instant | Medium | Tiered KYC | Low | Flexible deposits | Moderate |

| Crypto | Minutes | Low bank exposure | Exchange KYC | Irreversible | Offshore sites | Volatile |

| Prepaid vouchers | Instant | Lower direct tagging | Limited KYC | Non reversible | Deposit only use | Moderate |

Crypto reduces direct bank visibility but shifts exposure to exchange monitoring and blockchain traceability. Prepaid vouchers reduce merchant labeling but still require bank funding. Paytm remains one of the most stable rails in 2026 because it is deeply embedded in India’s digital economy.

How do offshore operators process Paytm deposits?

Offshore operators do not connect directly to Paytm as a gambling partner. They typically integrate through payment aggregators that rotate VPAs, QR codes, or merchant accounts. Licenses such as Curacao, Malta MGA, Anjouan, or Tuvalu regulate the operator side, but not the Indian payment rail. The payment routing often involves:

- Local aggregator onboarding

- Rotating UPI handles

- Merchant category masking

- Gateway based settlement batching

When an aggregator loses a banking partner, acceptance can disappear overnight. I have observed this repeatedly at major industry events such as ICE London and SiGMA, where operators openly discuss banking partner volatility in emerging markets. Therefore, Paytm availability reflects backend payment relationships rather than official gambling approval.

Does GST apply when using Paytm for betting deposits?

GST at 28 percent applies at the operator level on deposit value for real money gaming. Paytm does not separately deduct GST from the user, but operators factor it into wallet credit structures. The GST Council clarified that taxation applies to the full deposit amount rather than net gaming revenue. This significantly impacted operator economics beginning in late 2023.

For players, this means:

- Bonuses may shrink

- Cashback structures may change

- Deposit value may feel reduced in gameplay terms

The payment method does not change tax exposure. Whether using Paytm, Net Banking, or UPI, the GST obligation sits with the operator.

How can players reduce freeze risk when using Paytm?

Risk cannot be eliminated, but it can be reduced through predictable behavior and documentation clarity.

Practical steps:

- Complete full KYC on Paytm and the betting platform.

- Avoid rapid high frequency micro deposits.

- Maintain consistent deposit amounts.

- Avoid circular payment flows across multiple platforms.

- Use a secondary bank account instead of a salary account if concerned about transaction mixing.

- Monitor transaction history for unusual routing changes.

- Respond promptly to any compliance queries.

Secondary account strategies are commonly discussed in industry circles, not as evasion, but as transaction organization. Separating betting flows from salary inflows reduces anomaly detection.

Is Paytm better than prepaid vouchers for betting deposits?

Paytm offers higher operational stability, while prepaid vouchers reduce direct merchant labeling. Both remain traceable in different ways.

Prepaid vouchers:

- Are deposit only

- Cannot easily process withdrawals

- Require funding from a bank

Paytm casino:

- Supports both deposits and wallet transfers

- Is integrated with formal banking

- Requires full KYC for higher limits

For long term usability, Paytm is structurally more stable. Vouchers are tactical tools rather than complete payment solutions.

What documents might Paytm or banks request if transactions are flagged?

Banks may request:

- Identity confirmation

- Source of funds clarification

- Explanation of transaction purpose

- Income verification

These requests arise under RBI AML obligations. They are procedural rather than accusatory. During the compliance tightening of 2024, many users experienced temporary debit restrictions that were lifted once documentation was provided. Prompt cooperation is usually sufficient to restore account access.

Frequently Asked Questions About Paytm in India

Can I use Paytm to deposit on online casino and betting sites in India in 2026?

Yes, you can use Paytm if the betting site supports Paytm wallet payments or Paytm UPI transfers. Most deposits are processed through UPI infrastructure governed by NPCI and regulated under Reserve Bank of India oversight. The transaction is fully traceable through your linked bank account. Acceptance depends on the operator’s payment aggregator and can change if merchant accounts face compliance pressure or routing restrictions.

Can my Paytm wallet or bank account be frozen for betting deposits?

Yes, a freeze can occur if your transaction patterns trigger compliance alerts under RBI AML monitoring rules. Paytm operates within regulated payment frameworks, so unusual transfers to high risk merchant accounts may lead to temporary wallet or bank restrictions. Freeze risk typically depends on frequency, volume, and routing behavior rather than one isolated deposit, especially if transfers are repetitive or sudden.

Is Paytm safer than Google Pay or PhonePe for casino payments?

No, Paytm is not inherently safer because it often operates on the same UPI infrastructure as Google Pay and PhonePe. NPCI governs UPI rails, and banks apply monitoring under RBI compliance guidelines. Traceability is similar across all UPI apps. Risk exposure is shaped by transaction patterns, merchant classification, and account behavior rather than which app interface you choose.

Can I withdraw winnings directly to Paytm wallet?

Sometimes you can, but it depends on the operator’s withdrawal policy. Many betting platforms prefer sending payouts directly to your registered bank account instead of a wallet balance. Even if wallet withdrawals are supported, full KYC must be completed and the Paytm account name must match your betting profile. Withdrawal timing depends mainly on operator verification checks.

Why was my Paytm betting payment declined?

Most declines occur due to gateway restrictions, insufficient wallet balance, daily UPI limits, or internal compliance filters. Paytm may block certain merchant categories under its regulatory obligations. If the operator’s payment aggregator rotates or flags a virtual payment address, the transfer may fail even when your wallet and bank account are functioning normally.

Will my Paytm transaction show gambling on my statement?

Usually, it will not show a casino brand name directly. The transaction description often reflects a payment gateway, merchant code, or UPI virtual payment address. However, banks analyze transaction frequency, patterns, and merchant category indicators beyond simple text labels. Repeated similar transfers may still be identified during AML monitoring reviews.

Does GST apply when I deposit using Paytm?

Yes, GST at 28 percent applies at the operator level on the full deposit value for real money gaming, as clarified by the GST Council. Paytm does not deduct GST separately from your wallet. Instead, operators factor the tax impact into deposit credits, promotional structures, or bonus calculations, which can indirectly affect your usable balance.

Is it risky to use Paytm linked to my salary account?

It can be riskier if your Paytm wallet is directly connected to your primary salary bank account. Sudden or repeated transfers to unfamiliar merchant accounts may appear inconsistent with normal spending patterns. Banks monitor linked accounts under RBI AML frameworks, and irregular activity spikes can trigger temporary reviews or transaction restrictions.

How fast are Paytm deposits and withdrawals for betting sites?

Deposits are typically instant when processed through UPI or wallet transfer. Withdrawals can take several hours to a few days depending on operator internal risk checks and KYC verification. Payment speed is influenced more by compliance approval processes than by Paytm’s technical infrastructure, especially for larger payout amounts.

Does Paytm require full KYC for betting transactions?

Yes, full KYC is generally required for higher wallet limits and withdrawal eligibility. Paytm operates under RBI regulated payment norms that mandate identity verification for expanded usage. Betting operators also require separate KYC before releasing winnings. Any mismatch between your Paytm details and betting account information can delay or block withdrawals.

Can Paytm transactions trigger suspicious transaction reporting?

Yes, if transaction patterns resemble high risk activity under AML frameworks, banks and wallet providers may file suspicious transaction reports as required by RBI regulations. Such reporting does not automatically imply wrongdoing, but it increases scrutiny and may result in temporary account reviews while compliance teams assess transaction behavior.

Is Paytm more stable than prepaid vouchers for betting deposits?

Paytm is generally more stable because it is integrated directly with India’s regulated banking infrastructure. Prepaid vouchers reduce visible merchant tagging but still require bank funding at the purchase stage. Long term stability depends on payment aggregator relationships and regulatory climate rather than the payment brand alone.

Can I use Paytm for large betting deposits safely?

You can use Paytm for larger deposits, but higher amounts increase monitoring sensitivity. Wallet and UPI limits apply based on your KYC tier and bank policies. Consistent transaction behavior is important. Large sudden transfers or rapid repeated deposits are more likely to trigger compliance review under RBI AML systems.

Are Paytm payments reversible if I make a mistake?

Reversal is difficult once a wallet or UPI transfer is completed and settled with the operator. Unlike card payments, Paytm transactions typically do not support traditional chargeback protections. Disputes must be handled through customer support channels, and recovery depends on merchant cooperation rather than automatic banking mechanisms.

How does FEMA affect Paytm betting deposits?

Paytm transactions are domestic, but if merchant routing indirectly connects to offshore operators, banks may assess cross border exposure under FEMA guidelines. Retail users rarely face direct enforcement, yet unusual transaction flows linked to foreign entities can result in payment blocks or additional compliance review requests.

Is Paytm safer than crypto for casino deposits in India?

Paytm provides price stability and operates within India’s regulated banking environment. Crypto reduces direct bank exposure at the deposit stage but introduces exchange KYC requirements and blockchain traceability. Risk does not disappear with crypto; it shifts location. Compliance visibility exists in both systems through different monitoring mechanisms.

Why do some betting sites stop accepting Paytm suddenly?

Acceptance may change if the operator’s payment aggregator loses a banking partner or faces compliance pressure. Merchant accounts and UPI handles can be rotated or temporarily blocked. This often reflects backend payment routing adjustments rather than a technical issue with Paytm itself.

What documents might Paytm or my bank request if betting payments are flagged?

They may request identity verification, clarification of transaction purpose, or source of funds documentation. These requests arise from AML obligations under RBI guidelines. Providing accurate and consistent information typically resolves the review, and most restrictions are precautionary rather than permanent enforcement actions.

Can using Paytm reduce freeze risk compared to direct Net Banking?

Not necessarily. Paytm often routes transactions through UPI or linked bank accounts that remain visible under banking monitoring systems. The compliance risk depends on overall transaction behavior, volume, and frequency rather than whether you use a wallet interface or direct Net Banking transfer.

What is the biggest beginner mistake when using Paytm for betting?

The biggest mistake is assuming that a wallet provides anonymity. Paytm operates under RBI regulated frameworks and is linked to your verified identity. Another common error is depositing funds before confirming withdrawal rules and KYC requirements, which later leads to payout delays and compliance friction.

Final Analysis

Paytm is a regulated digital payment interface embedded within India’s formal financial system. It offers convenience and speed but does not remove compliance visibility under RBI oversight. Account freeze risk is tied to transaction behavior, not the app itself.

In 2026, informed payment decisions require understanding GST impact, banking monitoring patterns, and operator routing volatility. At JeetBetter, the goal remains simple: provide clarity so players can make responsible, financially aware choices in an evolving regulatory environment. Recommended online casino in Inida for Paytm deposits is: 10cric Casino

Top – Indian Casinos

150% Welcome Bonus up to ₹40,000

Welcome bonus offering 100% up to €600/$600

350% bonus of up to ₹70,300

Get 200% Welcome Bonus up to ₹1 Lakh + ₹500 Free Bet

Get 100% up to ₹25,000 bonus on your first deposit.

200% welcome bonus on their first deposit up to ₹1,00,000

Top Rated Casinos

200% welcome bonus on their first deposit up to ₹1,00,000

Get 200% Welcome Bonus up to ₹1 Lakh + ₹500 Free Bet

Get 100% up to ₹25,000 bonus on your first deposit.

150% Welcome Bonus up to ₹40,000

Welcome bonus offering 100% up to €600/$600

350% bonus of up to ₹70,300