Learn how to safely withdraw from Telegram Wallet to an Indian bank account. Expert advice on VDA taxes, TDS, P2P risks, and avoiding UPI blocks in 2026.

How to Withdraw Telegram Wallet to Indian Bank Accounts 2026

Opening Summary

Moving funds from the Telegram Wallet (@Wallet) to an Indian bank account in 2026 requires more than just a few taps; it requires a deep understanding of India’s Virtual Digital Asset (VDA) laws, FEMA regulations, and the technical nuances of the TON blockchain. This guide is for Indian users, from airdrop hunters to casual crypto holders, who need to “off-ramp” their Toncoin (TON) or USDT into INR without facing bank freezes or tax penalties. We will cover the legal status of the @Wallet, how to use UPI for Stars, and the safest step-by-step methods to move your money into the local banking system.

My Journey with the TON Ecosystem: Beyond the Chat App

When I first started exploring the Open Network (TON) integrated within Telegram, it felt like the “Wild West” of messaging. Fast forward to 2026, and the landscape has matured into a sophisticated financial layer. I’ve spent the last few years navigating the friction between decentralized global protocols and India’s rigid regulatory framework. In my experience, the biggest mistake users make isn’t a technical one; it’s a compliance one. They treat their Telegram Wallet like a private “black box,” unaware that the Income Tax Department now uses advanced AI-driven tools to cross-reference bank inflows with reported VDA transactions.

If you are looking to withdraw your funds, you aren’t just performing a transaction; you are interacting with a system that the Indian government now monitors closely as a transfer of digital assets. Let’s break down exactly how this works.

What is Telegram Wallet and How is it Being Used in India?

The Telegram Wallet, known by its handle @Wallet, is a custodial service built directly into the Telegram interface. Unlike non-custodial wallets (like Tonkeeper), where you hold your private keys, @Wallet manages the keys for you, making it incredibly accessible for beginners.

In India, the usage has skyrocketed due to the “Airdrop Summer” of 2024–2025. Projects like Notcoin and Hamster Kombat introduced millions of Indians to Toncoin. Today, users use the wallet for:

- Storing Airdrops: Collecting tokens from mini-apps and games.

- P2P Trading: Buying and selling USDT or TON directly with other users via UPI or IMPS.

- Remittances: Receiving small amounts of value from friends abroad, which is generally treated as a gift or remittance.

- Micro-payments: Using “Stars” to pay for digital goods and services within the Telegram ecosystem.

However, while the wallet itself is easy to use, moving those funds into INR triggers a series of legal and technical requirements that many overlook until their bank account is flagged.

Legal Status of the TON Blockchain and @Wallet in India (2026)

Is it legal? The short answer is yes, provided you follow the rules. As of 2026, the Indian government treats these transactions under the VDA framework.

The Tax Burden

You are legally required to pay a flat 30% tax on any gains made during the conversion, plus a 4% cess. The most critical thing I tell people is that the “No Set-off” rule is brutal: you cannot deduct gas fees or losses from one coin against the gains of another. For example, if your airdrop “landed” in your wallet at a value of zero (which the IT department often assumes), the entire withdrawal amount is treated as 100% profit.

The TDS Factor

Moving funds into INR via P2P or an exchange triggers a 1% Tax Deducted at Source (TDS) under Section 194S. If you use the Telegram P2P market, ensuring this TDS is paid is often your responsibility, or at least your risk. This is why I always recommend moving funds to an FIU-IND registered exchange like CoinDCX or WazirX before off-ramping. These platforms automate the 1% TDS, ensuring it reflects in your Form 26AS and preventing “unaccounted wealth” notices.

Buying Telegram Stars Using UPI

Before we talk about getting money out, let’s look at a popular way people put value in: Telegram Stars. Stars are the internal currency used to buy digital goods, access premium content, or support creators.

In India, the process is streamlined through the Google Play Store or Apple App Store, which allows you to use UPI (Google Pay, PhonePe, etc.).

- Step 1: Open a bot or channel offering digital goods.

- Step 2: Select the option to “Buy Stars.”

- Step 3: Choose your payment method. Since the mobile stores handle the transaction, your linked UPI ID will trigger a payment request.

- Step 4: Authorize the payment in your UPI app.

While this is convenient, remember that Stars are not “crypto” in the same way TON is; they are an in-app currency. You cannot easily “withdraw” Stars to a bank account. They are meant to be spent within the ecosystem.

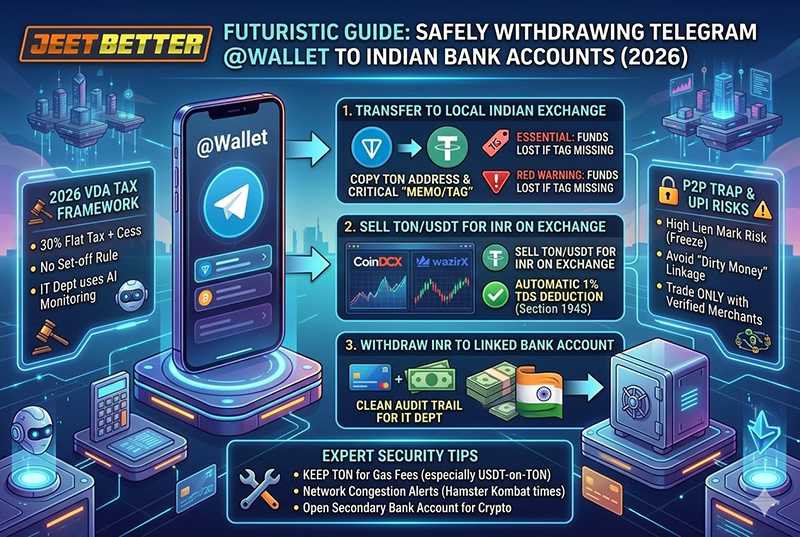

Step-by-Step for “Off-ramping”: Moving Assets to an Indian Bank

If you have TON or USDT in your Telegram Wallet and want it in your HDFC, ICICI, or SBI account, follow this “Safety First” route. This method avoids the high-risk P2P market where many Indian accounts get frozen.

Phase 1: Transfer to a Local Exchange

- Register on a Local Exchange: Use an FIU-registered platform (e.g., CoinDCX, WazirX, or Bitbns).

- Get Your Deposit Address: On the exchange, search for “TON” or “USDT (TON Network).” Copy the Deposit Address.

- The “Memo” or “Tag”: This is the most important part. Toncoin transactions require a “Comment” (Memo/Tag) to identify your specific account on an exchange.

- Execute the Transfer: In @Wallet, select “Send,” paste the address, and crucially, paste the Memo/Tag. If you forget the tag, your funds will be lost in the exchange’s pool account, and recovery is a nightmare.

Phase 2: Convert to INR

Once the tokens arrive on the local exchange, sell them for INR. The exchange will automatically deduct the 1% TDS.

Phase 3: Withdraw to Bank

Request an INR withdrawal to your linked bank account. This creates a clean “audit trail” that shows the source of funds is a regulated VDA platform rather than a random P2P individual.

The P2P Trap: Why UPI IDs Get Blocked

I’ve seen countless users lose access to their primary bank accounts because they tried to save 2% by using P2P. UPI blocks during Telegram P2P withdrawals usually happen because the buyer’s account is flagged for “cyber-fraud linkage”.

The National Payments Corporation of India (NPCI) now uses real-time monitoring that can freeze the entire payment chain. If you receive money from someone who even indirectly touched “dirty money,” your bank is mandated to place a Lien mark on your funds. This “freeze” stays until a Cyber Cell clearance is provided, which can take months.

How to Stay Safe if You Must Use P2P:

- Check Stats: Only trade with Verified Merchants with 1,000+ trades and a 98%+ rating.

- Avoid “New Joiners”: Scammers use “burner” accounts to offload tainted money into clean accounts like yours.

Document Everything: Keep screenshots of the trade agreement, the transaction hash, and the buyer’s profile. You’ll need these if you have to approach your Bank Manager with a formal letter.

Technical nuances and Troubleshooting

When withdrawing, you might see a “Pending” status for hours. This is usually due to network congestion on the TON blockchain or a low “Gas Fee” setting. High-traffic events, like a Hamster Kombat token launch, can spike costs.

Pro Tip: Always keep a small amount of Toncoin (TON) in your wallet to pay for “Gas”. I’ve seen many users fail their USDT withdrawals simply because they didn’t realize that USDT-on-TON still requires Toncoin for network fees.

Comparison: Direct P2P vs. Indian Exchange Off-ramping

| Feature | Telegram P2P Market | Indian Exchange (Safety Route) |

|---|---|---|

| Speed | Instant to 30 mins | 2 hours to 1 day |

| Bank Freeze Risk | High (Linked to “dirty money”) | Low (Regulated source) |

| Tax Compliance | Manual (User must track) | Automatic (1% TDS deducted) |

| Complexity | Low (Internal to Telegram) | Medium (Requires 2 platforms) |

| Fees | Lower (Market rates) | Higher (Withdrawal + Trading fees) |

| Proof of Funds | Hard to prove to IT Dept | Clear Transaction Report |

Final Thoughts on Security and Compliance

In 2026, the RBI’s updated KYC norms require banks to report any VDA-related inflows exceeding ₹50,000 per year to the Financial Intelligence Unit. There is no “anonymous” way to do this legally anymore.

My final piece of advice: Do not use your primary salary account for these transactions. Open a secondary savings account specifically for your crypto activities. This keeps your essential finances safe if a “Lien” is ever placed on your crypto-related account.

The TON ecosystem offers incredible opportunities, but in India, the “best” way to withdraw is always the one that keeps you on the right side of the law and the bank’s compliance team.

FAQ Answered by JeetBetter Experts

Is it legal to withdraw money from Telegram Wallet to my Indian bank account?

Yes, it is legal, provided you comply with the Virtual Digital Assets (VDA) tax laws and FEMA regulations. As of 2026, the Indian government treats these transactions as a transfer of digital assets. You are legally required to pay a flat 30% tax on any gains, plus a 4% cess. Additionally, moving funds to INR via P2P or an exchange triggers a 1% TDS under Section 194S.

Why is my UPI getting blocked when I try to sell USDT from Telegram?

UPI blocks often occur because the buyer’s account is flagged for “suspicious circular trading” or “cyber-fraud linkage”. In 2026, the NPCI monitors payments in real-time; if your buyer’s money is traced back to a scam, the entire chain, including your account, is frozen. Banks are legally mandated to place a “Lien mark” on your funds until you receive a Cyber Cell clearance, which is a lengthy process.

Can I transfer Toncoin directly to an Indian exchange to avoid P2P risks?

Absolutely, and this is the recommended “Safety First” route for 2026. By sending your TON or USDT from Telegram to a centralized Indian exchange like CoinDCX, you avoid dealing with anonymous P2P buyers. You simply copy your VDA deposit address and the required “Memo” or “Tag” from the exchange and paste it into the Telegram withdrawal screen. Once sold for INR on the exchange, the money is clean.

Why did my bank account get a “Lien” after a Telegram Wallet withdrawal?

A “Lien” or “Freeze” typically indicates that the money you received from a P2P buyer was part of a reported cybercrime, such as a “Digital Arrest” scam. Even if you acted honestly, if the buyer used “dirty money,” you are considered a “Layer 2” or “Layer 3” recipient. The bank’s compliance team freezes the account automatically once a victim reports fraud via the 1930 helpline.

How do I calculate the 30% tax on my Telegram airdrop withdrawals?

Airdrops are taxed at their Fair Market Value (FMV) at the time of receipt. If you received tokens worth ₹10,000 and they grew to ₹15,000 by the time you withdrew, you owe tax on the entire amount. Under the “No Set-off” rule, you cannot deduct gas fees. The Income Tax Department often treats the acquisition cost as zero, making the entire withdrawal amount taxable profit.

Is there a way to withdraw Telegram Wallet funds without a PAN card?

Legally, no. In 2026, any withdrawal ending up in an Indian bank account requires a PAN for tax compliance. Banks flag high-value UPI inflows that don’t match your income profile. Since 2025, the RBI requires banks to report VDA-related inflows exceeding ₹50,000 per year to the Financial Intelligence Unit (FIU). Using “No-KYC” groups is dangerous and can lead to Money Laundering (PMLA) charges.

What should I do if my Telegram Wallet withdrawal is “Pending” for hours?

“Pending” status is usually due to network congestion on the TON blockchain or low gas fees. In 2026, major token launches often cause transaction spikes. Check the TON Scan (tonviewer.com) using your wallet address to see if the transaction is on the blockchain. If it’s not there, it’s an internal Telegram bottleneck. Do not resend immediately to avoid double-debiting once the congestion clears.

How can I identify a “Fake Telegram Support” scammer during withdrawal?

Scammers often use official-looking names like “Wallet_Support_India” and message you first. They will claim your account is “locked” and ask for your 12-word Seed Phrase or a “verification deposit”. Remember: Telegram staff will never message you first or ask for your recovery phrase. Avoid clicking “WalletConnect” links from strangers, as these are often “Drainer Scams” that empty your wallet.

Does receiving Toncoin from international friends trigger FEMA issues?

Receiving assets from abroad is generally treated as a gift or remittance. However, under FEMA, if the value exceeds ₹50,000, it becomes taxable. Frequent transfers may be classified as “Commercial Trade,” and without proof of source, you risk being flagged for “unauthorized foreign exchange”. For transfers over ₹1 Lakh, keep a “Declaration of Gift” or an email trail to satisfy bank compliance.10. Why is my bank charging a “High-Risk Transaction” fee on Wallet withdrawals? While not always a direct “fee,” banks like HDFC and ICICI have implemented “Enhanced Monitoring” for VDA-related accounts. They may apply higher processing charges or restrict your digital limits to de-risk themselves from RBI penalties related to money laundering. To avoid this, don’t use your primary salary account; instead, use a secondary digital savings account for crypto activities to stay under the “High-Volume” radar.

Top – Indian Casinos

150% Welcome Bonus up to ₹40,000

Welcome bonus offering 100% up to €600/$600

350% bonus of up to ₹70,300

Get 200% Welcome Bonus up to ₹1 Lakh + ₹500 Free Bet

Get 100% up to ₹25,000 bonus on your first deposit.

200% welcome bonus on their first deposit up to ₹1,00,000

Top Rated Casinos

200% welcome bonus on their first deposit up to ₹1,00,000

Get 200% Welcome Bonus up to ₹1 Lakh + ₹500 Free Bet

Get 100% up to ₹25,000 bonus on your first deposit.

150% Welcome Bonus up to ₹40,000

Welcome bonus offering 100% up to €600/$600

350% bonus of up to ₹70,300